You got your salary credited. ₹30,000 in your account. By the 10th, rent is gone. By the 20th, groceries, travel, and a few online orders have eaten through most of what remained. By the 28th, you are checking your balance more than once a day.

If this sounds familiar, you are not alone — and more importantly, the problem is not your salary. The problem is the absence of a plan.

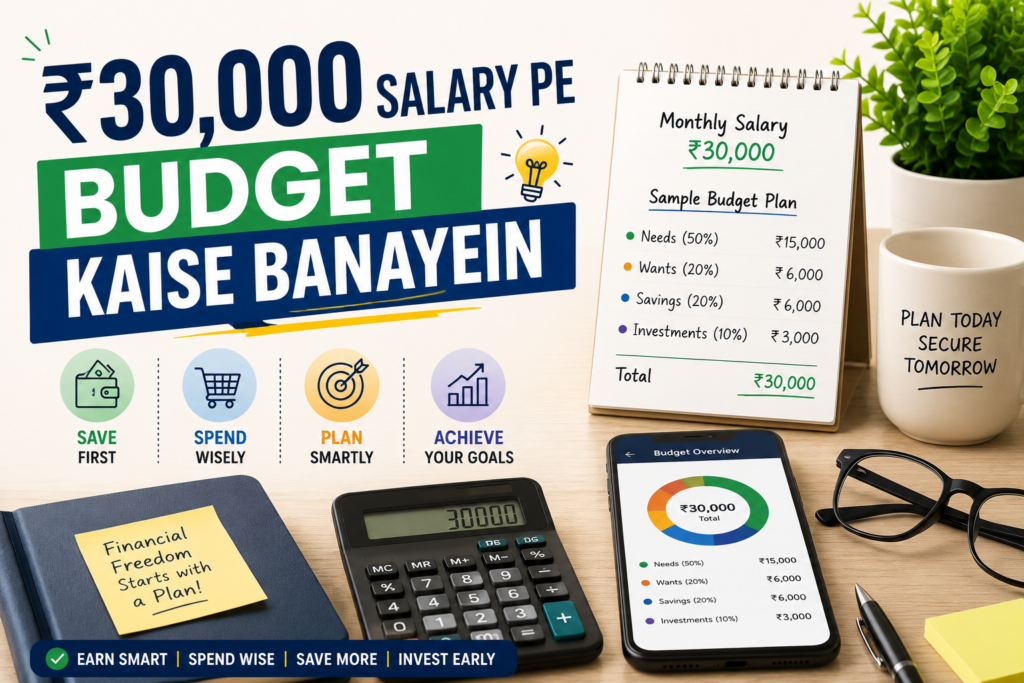

₹30,000 a month is not a lot of money in 2026, but it is enough — if you know where it goes and make deliberate decisions about it. This guide walks you through exactly how to build a monthly budget on a ₹30,000 salary, with real numbers, real categories, and a system that actually works in India.

Before you budget, you need to know what hits your account — not what your offer letter says. On a ₹30,000 gross salary, here is what typically happens before the money reaches you:

| Component | Amount |

|---|---|

| Basic Salary | ₹15,000 |

| HRA | ₹7,500 |

| Special Allowance | ₹6,000 |

| PF Deduction (Employee 12%) | — ₹1,800 |

| Professional Tax | — ₹200 |

| Actual In-Hand Salary | ₹26,500 – ₹28,000 |

The 50/30/20 rule is the most practical budgeting framework for salaried Indians. It is not perfect — no framework is. But it gives you a starting structure that you can adjust to your life. Here is how it divides your ₹27,000:

These are targets, not ceilings. If you live in a metro where rent is ₹12,000, your Needs bucket will naturally be higher. That is fine — adjust the Wants bucket down to compensate. The key is that your Savings bucket of 20% stays untouched regardless.

Fixed expenses are non-negotiable — they happen every month regardless of what you do. List them first so you know exactly how much of your ₹27,000 is already committed before you make any choices.

| Fixed Expense | Typical Amount (₹) |

|---|---|

| Rent — 1BHK, tier-2 city | ₹5,000 – ₹8,000 |

| Rent — PG or shared flat, metro | ₹6,000 – ₹10,000 |

| Mobile recharge | ₹300 – ₹500 |

| Internet (broadband) | ₹500 – ₹800 |

| OTT subscriptions | ₹200 – ₹500 |

| Loan EMI (if any) | Varies |

| Total Fixed (estimate) | ₹7,000 – ₹12,000 |

Variable needs are things you must spend on, but the amount changes every month. These go into your 50% Needs bucket alongside fixed expenses.

| Category | Monthly Target (₹) |

|---|---|

| Groceries & household essentials | ₹2,500 – ₹3,500 |

| Vegetables & daily items | ₹800 – ₹1,200 |

| Transport (bus / metro / petrol) | ₹1,500 – ₹2,500 |

| Medical / pharmacy | ₹300 – ₹500 |

| Personal care (soap, shampoo, etc.) | ₹400 – ₹600 |

| Total Variable Needs | ₹5,500 – ₹8,300 |

This is where most budgets collapse. Wants feel like needs. Zomato feels necessary. That Amazon order felt urgent at 11pm. Netflix, Spotify, a gym membership you use twice a month — each one feels small but together they silently drain your entire 30%.

₹8,100 is your wants budget. Here is how to split it realistically:

| Category | Monthly Budget (₹) |

|---|---|

| Eating out / food delivery | ₹1,500 – ₹2,000 |

| Shopping (clothes, accessories, online orders) | ₹1,000 – ₹1,500 |

| Entertainment (movies, events) | ₹500 – ₹800 |

| Personal spending / miscellaneous | ₹1,000 – ₹1,500 |

| Social spending (gifts, outings) | ₹500 – ₹800 |

| Total | ₹4,500 – ₹6,600 |

Most people save what is left after spending. That is exactly why most people never build wealth. The math does not work when saving is an afterthought.

The correct order is simple:

On salary day, the moment ₹27,000 hits your account, transfer ₹5,400 to a separate savings account or SIP. Do it before you pay rent. Before you pay anyone else. This is called paying yourself first — and it is the single habit that separates people who build wealth from people who intend to.

| Savings Allocation | Amount | Where to Park It |

|---|---|---|

| Emergency Fund (until 3 months salary saved) | ₹2,000 | Liquid mutual fund or high-interest savings account |

| SIP — Mutual Fund | ₹2,000 | Nifty 50 Index Fund or Flexi Cap Fund |

| Short-term goal (phone, travel, etc.) | ₹1,400 | Recurring Deposit or separate savings account |

| Total Savings | ₹5,400 | 20% of in-hand ✅ |

Rahul, a 24-year-old software tester from Pune earning ₹28,000 in-hand, was spending over ₹4,000/month on food delivery alone — without realising it. When he tracked his expenses for the first time using a free app, the number shocked him. He cut delivery orders from 20 a month to 6, switched to home-cooked meals on weekdays, and redirected ₹2,500 to his emergency fund. Within 8 months, he had ₹20,000 saved for the first time in his working life. His salary did not change by a single rupee. His awareness did.

A Real ₹27,000 Monthly Budget — Every Rupee Accounted For

Here is what a complete, realistic budget looks like in practice — not a theoretical framework, but an actual month-by-month plan:

| Category | Budget (₹) | Notes |

|---|---|---|

| Rent | ₹7,000 | 1BHK tier-2 city or shared PG room |

| Groceries + vegetables | ₹3,500 | Home-cooked meals, daily market |

| Transport | ₹1,800 | Metro pass + occasional cab |

| Mobile + internet | ₹700 | Prepaid + home broadband |

| Medical / misc essentials | ₹500 | Pharmacy buffer, personal care |

| Total Needs | ₹13,500 | 50% ✅ |

| Eating out / food delivery | ₹1,500 | Max 4–5 orders per month |

| Shopping (clothes, products) | ₹1,200 | Planned purchases only |

| Entertainment | ₹600 | Movies, OTT, events |

| Social / personal | ₹800 | Gifts, outings, celebrations |

| Miscellaneous buffer | ₹2,000 | Unexpected small expenses |

| Total Wants | ₹6,100 | Under 30% ✅ |

| Emergency Fund SIP | ₹2,000 | Liquid mutual fund |

| Mutual Fund SIP | ₹2,000 | Nifty 50 index fund |

| Short-term savings RD | ₹1,400 | Phone, travel, or goal fund |

| Total Savings | ₹5,400 | 20% ✅ |

| Grand Total | ₹25,000 | ₹2,000 buffer remaining every month |

What Happens If You Stay Consistent? The Numbers Are Motivating

If you invest just ₹2,000 per month in a Nifty 50 index fund at a 12% annual return — a conservative estimate for a 10-year horizon — here is what your money does while you sleep:

That is from ₹2,000 a month — less than the cost of one restaurant dinner per week. The math is not the hard part. Showing up every month is.

The 3 Biggest Budget Mistakes People Make on ₹30,000

1. Budgeting the gross salary, not in-hand

Your offer letter says ₹30,000. Your account receives ₹27,000. If you budget ₹30,000 and spend accordingly, you will be short every single month — not because you overspend, but because you started with the wrong number. Always budget what arrives in your account, nothing else.

2. Forgetting irregular expenses

Annual expenses — vehicle insurance, festival shopping, a cousin’s wedding gift, a new phone — feel like surprises because we do not plan for them monthly. Add up all your annual irregular expenses and divide by 12. That number becomes a fixed monthly line item in your budget. When the expense arrives, the money is already there.

3. Using a credit card without a repayment plan

A credit card on ₹30,000 salary is a powerful tool or a dangerous trap — depending entirely on whether you pay the full bill every month. Credit card interest in India runs at 36–42% per annum. A single month of carrying a balance can wipe out weeks of careful saving. Use a credit card only for expenses that are already in your budget, and set up auto-pay for the full amount.

Frequently Asked Questions

A ₹30,000 salary can support a stable, dignified life with real savings — if you decide what your money does before you spend it.

The 50/30/20 framework is not magic. It is a structure that replaces guesswork with intention. The first month will feel tight. The second month will feel normal. By the third month, the transfer on salary day will be automatic — mentally and literally.

Start this month. On the day your salary arrives, transfer your savings first. Track your spending for 30 days. Adjust what is not working. Repeat.

That is the entire system. The rest is just showing up.