Many people only think about their CIBIL score when they urgently need a loan. However, treating it as a cornerstone of your financial health, much like your savings, can open doors to incredible financial benefits. Proactively working to increase your CIBIL score is one of the smartest money moves you can make.

— Anshuman KumarWho this guide is for: If you’re a salaried Indian looking to understand and improve your creditworthiness, this guide is for you. Whether you’ve faced a loan rejection, been offered high interest rates, or simply want to strengthen your financial profile, you’ll find actionable steps here to increase your CIBIL score effectively.

Imagine this: You apply for your dream home loan or a much-needed personal loan. After weeks of waiting, you get the news – your loan is approved, but at a surprisingly high interest rate. Or even worse, your application is rejected outright. Often, the silent culprit behind such scenarios is your CIBIL score. Many salaried individuals in India face this exact situation without fully understanding why.

Your CIBIL score is more than just a three-digit number; it’s a reflection of your financial discipline. Banks and lenders use it as a primary factor to assess your creditworthiness. A higher score means you are a lower risk, translating into better loan offers, lower interest rates, and easier approvals. Therefore, learning how to increase CIBIL score is absolutely essential for your financial future.

Understanding Your CIBIL Score: The Gateway to Better Loans

The CIBIL score, ranging from 300 to 900, is India’s most prominent credit score. It’s generated by TransUnion CIBIL, one of India’s four credit bureaus. Banks and Non-Banking Financial Companies (NBFCs) regularly report your credit activities to these bureaus. This includes your loan repayments, credit card usage, and even loan inquiries.

A strong CIBIL score tells lenders that you are responsible with credit. Conversely, a low score suggests potential risk. This makes it harder to secure credit, or you might end up paying significantly more in interest over the loan tenure. Understanding this baseline is your first step towards improving it. Moreover, your financial health directly hinges on this number.

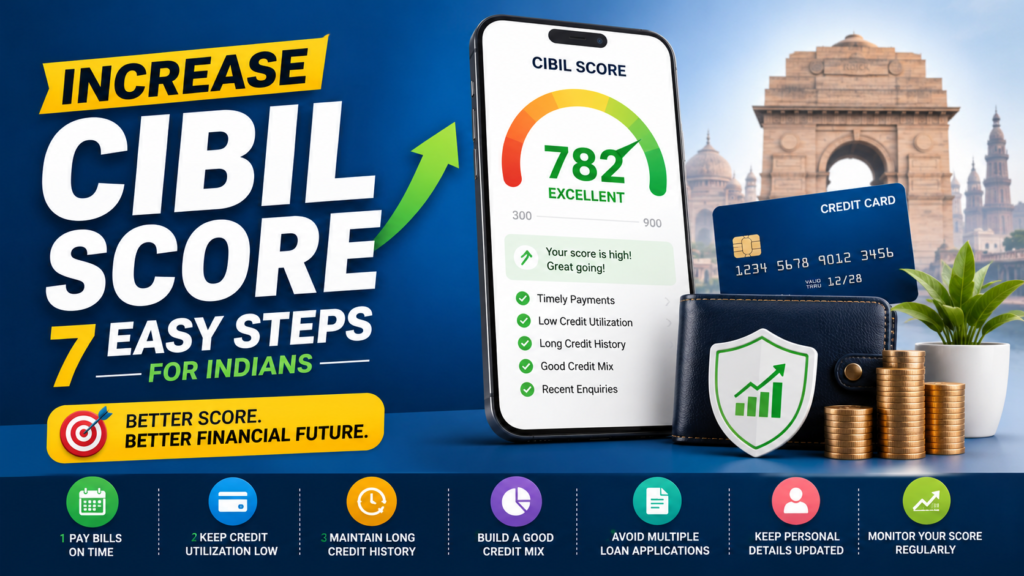

Practical Steps to Increase Your CIBIL Score

Improving your CIBIL score isn’t an overnight process. It requires consistent effort and smart financial habits. However, with the right strategy, you can see significant improvement over time. Here are seven effective steps salaried Indians can take to actively increase CIBIL score and build a stronger financial profile:

This is arguably the most critical factor. Payment history accounts for about 30% of your CIBIL score. Even a single missed payment can significantly hurt your score. Therefore, always prioritize timely repayments. Set up auto-debits for your EMIs and bill payments to avoid accidental defaults. This simple habit will dramatically help you increase CIBIL score over months.

Your credit utilisation ratio (CUR) is the amount of credit you’re using compared to your total available credit limit. For example, if your credit card limit is ₹1,00,000 and you spend ₹30,000, your CUR is 30%. Lenders prefer a CUR below 30%. High utilisation signals that you might be over-reliant on credit. Try to keep your credit card outstanding balances well below your limit to effectively increase CIBIL score.

Each time you apply for a new loan or credit card, a ‘hard inquiry’ is made on your credit report. Multiple hard inquiries in a short period can be seen as a sign of financial distress and can lower your CIBIL score. Be selective with your credit applications. Research different loan options using tools like our Personal Loan Calculator before making multiple applications.

Having a mix of secured loans (like home loans or car loans) and unsecured loans (like personal loans or credit cards) can positively impact your score. It shows lenders that you can manage different types of credit responsibly. However, don’t take out loans just for the sake of improving your mix. Only borrow what you genuinely need. A good credit mix helps to increase CIBIL score gradually.

Older credit accounts, especially those with a perfect payment history, demonstrate your long-term creditworthiness. Closing them can reduce your overall available credit, thereby increasing your credit utilisation ratio and potentially lowering your score. Keep older accounts open, even if you use them sparingly, to maintain a longer credit history and help increase CIBIL score.

Mistakes can happen. Incorrect reporting by lenders, identity theft, or data entry errors can negatively affect your score without your knowledge. You are entitled to one free CIBIL report annually. Review it thoroughly for any discrepancies. If you find errors, dispute them immediately with CIBIL and the concerned lender. Correcting these can quickly help to increase CIBIL score.

When you co-sign a loan or act as a guarantor, that loan also appears on your credit report. If the primary borrower defaults on payments, it will negatively impact your CIBIL score as well. Only co-sign for someone you trust completely and are confident will make timely payments. This is a significant responsibility that can directly affect your ability to increase CIBIL score.

Common CIBIL Mistakes Salaried Indians Make

While striving to increase your CIBIL score, it’s equally important to be aware of the pitfalls. Many salaried professionals, despite their best intentions, inadvertently make choices that harm their credit profile. Avoiding these common mistakes can save you a lot of trouble and keep your score healthy.

Real Story: How Rajesh From Mumbai Boosted His CIBIL Score

Rajesh, a 32-year-old software engineer from Mumbai, found himself in a tough spot. He wanted to buy a new car worth ₹12 lakhs, but his loan application was rejected due to a CIBIL score of 630. He had an old personal loan where he had missed a couple of EMIs, and his credit card was often maxed out. Realizing he needed to increase CIBIL score urgently, he decided to take action.

Rajesh first obtained his CIBIL report. He saw the missed payments and the high credit card utilisation. He immediately started by paying off his credit card balances completely each month. He also set up auto-debit for his personal loan EMIs to ensure no more defaults. Over the next six months, he consciously limited his credit card usage, keeping it below 20% of his limit.

He also contacted the bank for the old personal loan to ensure all records were correctly updated. After a consistent 8 months of disciplined financial behaviour, Rajesh’s CIBIL score climbed from 630 to a respectable 765. He reapplied for the car loan, got approved, and even secured a lower interest rate, saving him roughly ₹45,000 over the loan tenure. His determination to increase CIBIL score paid off!

Do’s and Don’ts for a Healthier CIBIL Score

To further simplify your journey to a better CIBIL score, here’s a quick reference of what you should and shouldn’t do:

- ✅ Pay all your EMIs and credit card bills on or before the due date.

- ✅ Keep your credit card utilisation below 30% of your total limit.

- ✅ Check your CIBIL report annually for free and dispute any errors.

- ✅ Maintain a healthy mix of secured and unsecured credit over time.

- ✅ Set up reminders or auto-payments for all your credit commitments.

- ❌ Miss or delay payments, even by a few days.

- ❌ Max out your credit cards consistently.

- ❌ Apply for multiple loans or credit cards in a short span.

- ❌ Close old credit card accounts with good payment history.

- ❌ Co-sign a loan without fully understanding the risks involved.

Frequently Asked Questions About Increasing CIBIL Score

Your CIBIL score is a powerful tool in your financial journey as a salaried Indian. It determines not just if you get a loan, but also how much you pay for it. By understanding the factors that influence it and consistently applying the strategies discussed, you can effectively increase your CIBIL score.

Remember, building a strong credit profile is a marathon, not a sprint. Be patient, be diligent, and keep an eye on your financial habits. A higher CIBIL score opens doors to better financial opportunities, helping you achieve your dreams faster and more affordably.